Shares for the future: a top 5 stock that’s ‘absurdly cheap’

One of the highest-scoring companies that analyst Richard Beddard covers, its modest valuation and large cash pile imply it’s a good long-term investment.

17th January 2025 15:04

by Richard Beddard from interactive investor

After two years of reduced profit, Dewhurst Group (LSE:DWHT) returned to growth in the year to September 2024.

The lift component supplier has weathered a period of disrupted supply and inflation. Headwinds persist, but it is in a very strong financial position.

- Invest with ii: Top UK Shares | Share Tips & Ideas | Cashback Offers

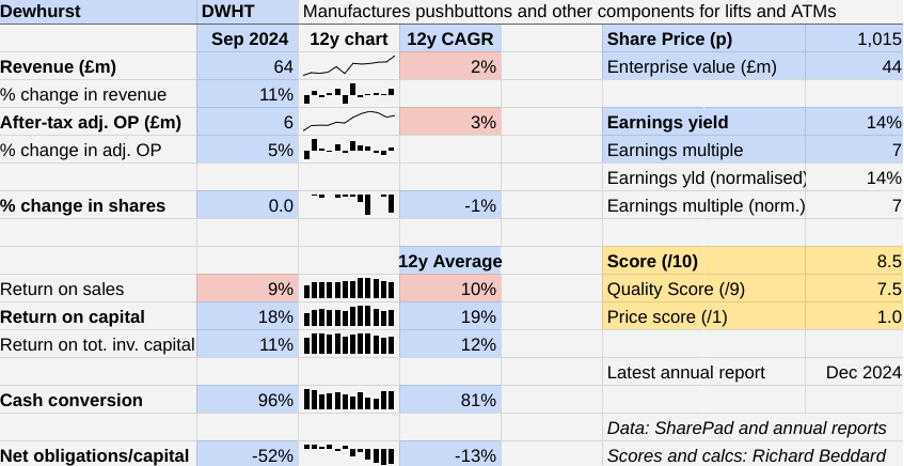

Scoring Dewhurst: slow growth

With a long track record of high and stable returns, Dewhurst is in many respects a highly successful business.

The Past (dependable) [2.5]

- Profitable growth: Modest historical growth [0.5]

- Strong finances: Net cash, strong cash flows [1]

- Through thick and thin: Lowest return on capital (RoC) 17% (2017, 2023) [1]

Modest profit margins, typically about 10%, reflect the mix of manufacturing, distribution, and installation work.

The most significant blot on Dewhurst’s financial record is past revenue and profit growth. It is in low single-digit percentages, compounded over the last 12 years.

Even in the worst year of the last 12 though, Dewhurst achieved a 17% return on capital, and the resulting cash is piling up on its balance sheet.

In 2024, Dewhurst used some cash to invest in a newly acquired display factory in Singapore. It also bought out the remaining 25% of the shares in P&R lift cars. P&R is an Australian subsidiary that designs, manufactures and installs lift interiors.

Dewhurst returned money to shareholders by buying back some non-voting shares. It also made additional payments into its defined benefit pension scheme.

At the end of the financial year, the value of the pension scheme’s assets outweighed the value of its obligations. Eventually, the company intends to transfer the scheme to an insurer. This would remove the impact of fluctuations in its value on the company’s balance sheet, and the administrative burden of running it.

If this happens, Dewhurst’s already decent cash conversion should improve, increasing its ability to return cash to shareholders, invest in the business and fund acquisitions.

The short-term outlook is cloudy. In the UK, where Dewhurst earned 31% of revenue in 2024, the economy is sputtering. The US business may have to contend with tariffs on lift products imported from Dewhurst’s factories in the UK and Canada.

Dewhurst earned 24% of revenue from the Americas in 2024, much of it in the US.

The Present (distinctive) [3]

- Discernible business: Long-established supplier of lift components [1]

- With experienced people: Very [1]

- That creates value for customers: Quality, service [1]

Dewhurst primarily supplies lift components. It manufactures push buttons, displays, lift car operating panels and hall lanterns, distributes lift components and electrical and safety equipment, and fits out lift interiors.

The lift business is well represented throughout the Anglosphere, with long established subsidiaries in the US and Canada, and more recently acquired subsidiaries in Australia.

Two very small subsidiaries make bollards and other furniture for roads and cyclepaths, and keypads for ATMs, a business that is in decline.

Dewhurst’s reputation for quality, service and stability has been achieved under the management of Richard and David Dewhurst who stood back from day-to-day management in 2022. The newish chief executive is John Bailey, who joined when Dewhurst acquired A&A, a distributor, in 2018. He had been at A&A since 2008.

In something of a job-swap, chief transformation officer Jeremy Dewhurst has stepped up into the board and taken the chief financial officer role from long-standing incumbent Jared Sinclair. Sinclair remains on the board as chief innovation officer.

Jeremy Dewhurst owns 10% of the shares. Richard Dewhurst, non-executive chair, owns 15%. David Dewhurst, also a non-executive director, owns 13%. Other family members own substantial shareholdings, and work in the business.

Their ownership suggests Dewhurst will continue to be run conservatively for the long term.

The Future (directed) [2]

- Addressing challenges:Advances in technology, mature markets [0.5]

- With coherent actions: Innovation, acquisitions [0.5]

- That reward all stakeholders fairly: Long-term ethos, employee friendly [1]

Even lifts are subject to technological disruption. Although pushbuttons still have a place, because everybody can use them and they are extremely hard wearing, they are gradually giving way to LCD displays. This is especially true in high footfall locations and areas where multiple lifts are controlled by destination dispatch systems.

Dewhurst has long bought displays and assembled them into operating panels also incorporating Dewhurst pushbuttons and other components. In 2023, though, it acquired display technology and a factory in Singapore from one of its suppliers.

Patience and opportunism define Dewhurst’s strategy. For example, in recent years it has often acquired Australian firms rather than North American or UK subsidiaries because they tend to be cheaper.

- Victoria shares: new forecasts from bullish analyst

Sign up to our free newsletter for investment ideas, latest news and award-winning analysis

This year, Dewhurst shifted some of its lift product assembly work from the UK to its ATM keypad factory in Hungary, which has spare capacity. It also introduced an e-commerce system at Lift Material, an Australian distributor. The system was developed at A&A, the UK distributor, which already had sophisticated e-commerce capabilities.

To my mind Dewhurst’s owners and managers have always fostered an employee-focused culture.

Since the pandemic though, the company has formalised employee relations by instituting a regular staff survey and rolling out a global HR system.

The statistics they are generating are encouraging. In 2024, employee engagement increased from 79% to the company’s target of 85% and employee turnover fell from 13% to 11%, below Dewhurst’s target rate of 15%.

After trials, it has introduced four-day work weeks at two of its smaller subsidiaries.

The price (discounted?) [1]

- Yes. A share price of £10.15 values the enterprise at about £44 million, 7 times normalised profit.

A score of 8.5 implies Dewhurst is a good long-term investment.

Dewhurst’s ponderous historic growth rate and mature markets are off-putting, but the company’s cash pile gives it options. Meanwhile, the shares are absurdly cheap.

It is ranked 5 out of 40 shares in my Decision Engine.

24 Shares for the future

Here is the ranked list of Decision Engine shares. I review the scores at least once a year, soon after each company has published its annual report. The price scores are calculated using the share price prior to publication.

Generally, I consider shares that score 7 or more out of 10 to be good value. Shares that score 5 or 6 out of 10 are probably fairly priced.

Hollywood Bowl Group (LSE:BOWL), Renew Holdings (LSE:RNWH), RWS Holdings (LSE:RWS) and Victrex (LSE:VCT) have all published annual reports and are due to be re-scored.

0 | Company | * | Description | Score |

1 | Manufactures tableware for restaurants and eateries | 10.0 | ||

2 | Supplies kitchens to small builders | 9.1 | ||

3 | Imports and distributes timber and timber products | 9.0 | ||

4 | Makes light fittings for commercial and public buildings, roads, and tunnels | 8.7 | ||

5 | Dewhurst | Manufactures pushbuttons and other components for lifts and ATMs | 8.5 | |

6 | Distributor of protective packaging | 8.4 | ||

7 | Manufactures computers, battery packs, radios. Distributes components | 8.3 | ||

8 | Manufacturer of scientific equipment for industry and academia | 8.2 | ||

9 | Flies holidaymakers to Europe, sells package holidays | 8.0 | ||

10 | Designs recording equipment, loudspeakers, and instruments for musicians | 8.0 | ||

11 | Sells hardware and software to businesses and the public sector | 7.9 | ||

12 | Whiz bang manufacturer of automated machine tools and robots | 7.6 | ||

13 | Manufactures/retails Warhammer models, licences stories/characters | 7.6 | ||

14 | Manufactures PEEK, a tough, light and easy to manipulate polymer | 7.5 | ||

15 | Distributes essential everyday items consumed by organisations | 7.5 | ||

16 | Manufactures filters and filtration systems for fluids and molten metals | 7.4 | ||

17 | Sells promotional materials like branded mugs and tee shirts direct | 7.4 | ||

18 | Operates tenpin bowling and indoor crazy golf centres | 7.3 | ||

19 | Manufactures surgical adhesives, sutures, fixation devices and dressings | 7.3 | ||

20 | Manufactures vinyl flooring for commercial and public spaces | 7.3 | ||

21 | Online marketplace for motor vehicles | 7.2 | ||

22 | Surveys and distributes public opinion online | 7.1 | ||

23 | Repair and maintenance of rail, road, water, nuclear infrastructure | 7.1 | ||

24 | Translates documents and localises software and content for businesses | 7.0 | ||

25 | Online retailer of domestic appliances and TVs | 6.8 | ||

26 | Sources, processes and develops flavours esp. for soft drinks | 6.8 | ||

27 | Acquires and operates small scientific instrument manufacturers | 6.7 | ||

28 | Manufactures natural animal feed additives | 6.7 | ||

29 | Retails clothes and homewares | 6.7 | ||

30 | Supplies vehicle tracking systems to small fleets and insurers | 6.6 | ||

31 | Publishes books, and digital collections for academics and professionals | 6.2 | ||

32 | Manufactures military technology, does research and consultancy | 6.1 | ||

33 | Casts and machines steel. Processes minerals for casting jewellery, tyres | 5.7 | ||

34 | Manufactures sports watches and instrumentation | 5.5 | ||

35 | Manufactures power adapters for industrial and healthcare equipment | 5.5 | ||

36 | Manufactures disinfectants for simple medical instruments and surfaces | 5.3 | ||

37 | Makes marketing and fraud prevention software, sells it as a service | 5.2 | ||

38 | Runs a network of self-employed lawyers | 4.8 | ||

39 | Develops and manufactures hygiene, baby, and beauty brands | 4.5 | ||

40 | Manufactures specialist paper, packaging and high-tech materials | 3.8 |

Scores and stats: Richard Beddard. Data: SharePad and annual reports

Click on a share's name to see a breakdown of the score (scores may have changed due to movements in share price)

Shares marked with an asterisk (*) have been re-scored, click the asterisk to find out why.

Richard Beddard is a freelance contributor and not a direct employee of interactive investor.

Richard owns Dewhurst and many shares in the Decision Engine. He weights his portfolio so it owns bigger holdings in the higher-scoring shares.

For more on the Decision Engine, please see Richard’s explainer.

Contact Richard Beddard by email: richard@beddard.net or on Twitter: @RichardBeddard

AIM stocks tend to be volatile high-risk/high-reward investments and are intended for people with an appropriate degree of equity trading knowledge and experience.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.

Disclosure

We use a combination of fundamental and technical analysis in forming our view as to the valuation and prospects of an investment. Where relevant we have set out those particular matters we think are important in the above article, but further detail can be found here.

Please note that our article on this investment should not be considered to be a regular publication.

Details of all recommendations issued by ii during the previous 12-month period can be found here.

ii adheres to a strict code of conduct. Contributors may hold shares or have other interests in companies included in these portfolios, which could create a conflict of interests. Contributors intending to write about any financial instruments in which they have an interest are required to disclose such interest to ii and in the article itself. ii will at all times consider whether such interest impairs the objectivity of the recommendation.

In addition, individuals involved in the production of investment articles are subject to a personal account dealing restriction, which prevents them from placing a transaction in the specified instrument(s) for a period before and for five working days after such publication. This is to avoid personal interests conflicting with the interests of the recipients of those investment articles.